CCB provides next-day availability for most deposits while reserving the right to impose holds on particular checks. The three main types of holds are:

- Case-by-case – 2-Day Holds

- Exception hold – 7-Day Holds

- New account hold – 9-Day Holds

When placing a hold, ensure the number of days for the hold matches the time period for the hold type chosen. The length of the hold must be in compliance with the Permanent Funds Availability schedule. See the Funds Availability chart and the Funds Availability calculator for more information.

For detailed procedures and information about Alert Center, see Placing a Hold.

Same-Day Availability (No Hold)

Federal government Automated Clearing House (ACH) payments must be available the day they are received by the bank. Note: This is not required by Regulation CC (Reg CC), but it is a membership condition by the Federal ACH.

Next-Day Availability (No Hold)

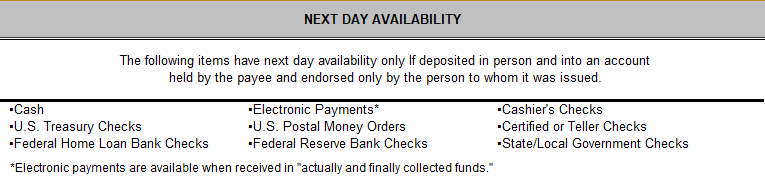

The items described in this section are defined as next-day items. These items are considered "good funds:" Next Day holds apply to the following:

Cash

This Includes cash deposits made at proprietary Automated Teller Machines (ATMs) prior to the posted cut-off time.

Electronic Payments

- This includes an Electronic Funds Transfer that has been received in unconditional form. Note: Federal ACH payments are required to be same-day items, as a condition of membership in the Fed ACH.

- Wire transfers that are unconditionally received.

Negotiable Instruments

Negotiable instruments have next-day availability only if such items are initially payable to the depositor on the face of the check and are deposited at one of the staffed facilities into an account held by the payee. Note: This does not include third-party checks that are payable to the depositor by endorsement.

The following checks are considered negotiable instruments:

- U.S. Treasury checks

- U.S. Postal money orders

- State or local government checks

- Cashier checks, Certified checks, and teller checks

- Federal Reserve Bank and Federal Home Loan Bank checks

U.S. Treasury Checks

Payable to the depositor, which must be deposited at a proprietary ATM.

On-Us Checks

An on-us check is any item drawn on a CCB account. On-us checks are next-day items for established clients, but do not have to be next-day items for new clients.

Given the current state of technology, with color copies capable of reproducing documents such as checks with tremendous fidelity and PCs with all kinds of graphic capabilities and reproduction capabilities, associates must always consider that official bank checks or government checks may be copies or forgeries, and be alert for large items that should receive extra attention and possibly exception holds.

Tip: Official bank checks are always produced in multiple parts that have to be separated. There is always a perforation line on such checks. Official bank checks must always be printed on safety paper with a watermark. Forgeries and reproductions of such checks will not have the perforation, and will not have a watermark, which cannot be reproduced by the copier.

Case By Case 2-Day Hold

Funds must be available on the second business day after the date of deposit. Exception holds can be placed on these items for longer periods of time, up to 7 business days.

Local Checks

Local checks include all checks drawn on financial institutions in the United States and possessions.

The following can be considered for a case-by case hold:

- If the check amount is significantly greater than the account balance

- If the client acts suspicious

- When the bank acts in good faith

When case-by-case holds are placed, no specific reason is needed for processing; however, a reason must be provided to the client. Each associate should use this verbiage when placing this type of hold: "The deposited check is uncollected funds." This is true of all checks deposited.

2-Day Hold

A 2-day hold is placed on the next day available items including U.S. Treasury checks, cashier checks, certified or teller checks, U.S. postal money orders, local and state government checks.

The following applies for 2 Day Holds:

- These items are not payable to the CCB depositor on the face of the check.

- These items are not deposited at a CCB staffed facility into an account held by the payee.

- State or local government checks are deposited in a bank outside the state where the check is issued.

- The reason for the hold is Other. One of the following descriptions is required:

- Not deposited in person

- Not payable to the depositor

- State or local government checks deposited in a bank outside the state where the check is issued

By definition, all U.S. Treasury checks and U.S. Postal money orders must be treated as local checks. At the option of the bank, any check (other than a Treasury check), payable to the depositor, which is deposited at a proprietary ATM, can be considered to be a two-day item. Treasury checks payable to the depositor must still be given next-day availability.

First $225 Rule (2-Day Hold)

The first $225 of the total deposit of any items (such as local checks) must be made available to the depositor on the next business day. When this rule applies, the bank can decide which items to apply this exception to. This rule also does not apply if the bank gives cash back to the depositor of $225 or more. The balance of the funds must be available according to the funds availability schedule.

The first $225 rule does not apply when a 2-day hold is placed on items described as "next day" items. The hold is placed on the full amount.

This rule does not apply to accounts that are overdrawn (OD) less than $225 at the time a deposit is made. If an account is OD less than $225, they will get partial benefit from the rule. (For example: If the account is OD $175, the client gets next-day availability of $50 or more unless the account is one with repeated ODs then the bank can decide to impose a safeguard hold).

Exception Holds (7 Day Hold)

Exception holds add additional days to the hold time due to the added risk to the bank. When placing an exception hold, you must have a specific reason for extending the hold time period. The funds must be available on the seventh business day after the date of the deposit. Exception holds can be divided into two categories:

- Safeguard exception hold

- Reasonable cause exception hold

First $ 225 Rule

With the exception of the large deposit exception hold, exception holds do not get the benefit of the first $225 availability rule.

Safeguard Exception Hold

Safeguard holds require a reason for which the hold is placed and this reason must be disclosed on the hold notice. Safeguard holds are specifically defined in the regulation to include:

- Large deposit exception hold

- Redeposit of a returned item

- Repeated OD account deposit

- Emergency situation

Large Deposit Exception Hold

A large deposit exception hold is placed when checks deposited on this day exceed $5,525.

When deposits are in excess of $5,525 on any one day, the amount in excess of $5,525 may be held for a longer period of time. A large deposit hold is subject to the first $225 rule. When choosing this reason, the associate is actually placing two holds.

The 1st $5,525 will be held following the funds availability schedule for case-by-case holds. Any amount above $5,525 will be held for a longer time frame. When placing a large deposit exception hold, the associate must make the following funds available:

- $225 next day

- $5,300 on the 2nd day

- Any amount above $5,525 on the 7th day

Redeposit of Returned Item

Any item that is returned due to a recently unpaid deposited check is subject to a redeposit of returned item hold. This hold does not receive the 1st $225 Rule. If the actual check being deposited has been returned due to non-sufficient funds (NSF) or uncollected funds, an exception hold can be placed.

Repeated OD Account Deposit

Repeated OD account holds occur when a client has overdrawn their account repeatedly in the last six months.

This hold does not receive the 1st $225 Rule. An account can be considered to have repeated OD if one of the following occurs:

- The account had an OD balance on six or more days in the past six months

- If an account is OD by $5,525 or more for two or more days in the last six months

- If an account would be OD by $5,525 if all presented items had been paid

Emergency Hold

Emergency holds occur when an emergency such as failure of communications or computer equipment has occurred. This hold applies when an emergency occurs during processing (either at the paying bank or depository bank) such as a flood, loss of power, or computer malfunction.

An emergency hold is not subject to the 1st $225 Rule.

Reasonable Cause Exception Hold

Reasonable cause exception holds protect the bank from the risk of loss due to various circumstances. To qualify for a reasonable cause exception hold, the bank, acting in good faith, must have some reason to believe an item may not be paid when it is presented. The reason for such a hold must be disclosed on the hold notice. Reasonable cause holds are not subject to the 1st $225 Rule.

Reasons for a reasonable cause exception hold include:

- The bank has received notice that the check is being returned unpaid.

- The bank received information that indicates the check may not be paid.

- The check is drawn on an account with repeated overdrafts.

- The bank is unable to verify the endorsement of a joint payee.

- The information on the check is inconsistent.

- There are erasure marks or other apparent alterations on the check.

- The routing number of paying bank is not a current ABA#.

- The check is postdated or stale dated.

- Information from the paying bank indicates the check may not be paid.

- We have been notified the check has been lost or damaged.

Time Extension for Exception Holds

If an associate is placing a safeguard or a reasonable cause exception hold on a local check or a next day item, the hold time is extended past the hold period of a case-by case hold, as defined in the funds availability schedule. Longer holds may be reasonable, under some circumstances, but the bank is prepared to justify the delay if the client complains to the government.

New Account Holds (9 day Hold)

Historically there is a greater chance of fraud on a new account. Special rules for deposits made by a new client allow us to impose longer holds for the first 30 days after an account is opened. Deposit items must be available on the 9th business day after the date of deposit. Associates must place new accounts on hold that are open for less than 30 days.

As a limited exception, a newly opened account is not a new account if each owner has had another transaction account (demand deposit account (DDA) or negotiable order of withdrawal (NOW) account) at the bank for at least 30 days prior to opening the new account. New accounts do not qualify for the 1st $225 Rule.

The funds must be available on the 9th business day after the date of deposit.

Credit must be given for the first $5,525 of Treasury checks and other next-day items with the amount in excess of $5,525 to be available on the 9th business day. As a special rule, we must give next-day availability for the first $5,525 of traveler's checks and other next-day items. Note: This rule applies only to new clients, and is the only instance in which new clients have to receive treatment that is more favorable than that of existing clients.

On-us checks are not specifically addressed in the regulation for new clients, except that they are not required to be treated as next-day items. If a client is depositing large on-us checks, a two-day hold should be adequate to determine funds. As an alternative, the Teller could cash out the check and deposit the cash and no hold would be required.

Hold Notices

Regulation CC requires that the client receive a notice whenever funds are held. Specific rules regarding when the client is to be notified have been established.

When To Give Holds

Associates use one of two Reg CC hold notice forms when placing holds. Reg CC hold notice forms include:

- System Generated Notice of Delayed Availability form

- Manual (handwritten) Notice of Hold form.

Note: A copy of one of the Reg CC hold notice forms must be given to the client.

Holds placed When Client is Present

Associates must always give the client the hold notice while they are at the teller window or associate desk.

When providing a client with a hold notice, do the following:

- Obtain the client signature on the notice as an acknowledgment of the hold.

- If there is no signature line on the notice, a signature anywhere on the page is sufficient.

- If the client refuses to sign, note the refusal on the form stating the following, "Notice provided, depositor failed to sign the notice."

- Explain to the client that their refusal to sign does not negate that a hold was placed.

- Associate initials are required at the top of the notice.

Holds Placed When a Client is Not Present

If the decision to place the hold is made after the transaction has processed and the client has left the office, or the item being held is received through the mail, ATM, night drop, or courier, a hold notice is to be mailed to the client within 24 hours.

The associate places their initials and office location at the top of the notice. The associate must write "Mailed to Client on XX/XX/20XX" on the client signature line or in a blank area on the form.

Note: If the bank finds it appropriate to extend or change a hold previously placed, associates are required to submit a new notice to the client.

Best Practice: Associates are required to provide a reason for the hold. The reason must match the number of days held. Associates must always choose the correct reason for the hold.

- It is critical to choose the correct number of days (according to Reg CC) when placing a hold

- It is critical to enter the correct number of days when producing the Notice of Delayed Availability form

Placing A Hold

When an associate has determined that a hold is needed for an item being cashed or deposited, the associate must either print a Notice of Delayed Availability or complete the pre-printed Capital City Bank notice of hold form for the client.

A Personal Banker or CXM/ CXMII is responsible for the following:

- Loading and uploading holds in the system and printing the Notice of Delayed Availability form for a new deposit account holder and/or any other hold a Personal Banker may deem necessary

- Completing a pre-printed Notice of Hold when the operating system is not available. The hold must be uploaded when the system becomes available.

- If the teller system is not available, load all holds in Silverlake.

- It is critical to use the correct expiration date, which is the date available that is printed on the Notice of Delayed Availability.

- The expiration date of the hold is the processing date prior to the available date.

- When funds are to be available on a Monday, the expiration date must be the previous Friday. CCB does not process holds on Saturday or Sunday.

A Teller is responsible for the following:

- Processing the transaction

- Uploading the hold to the client's account

- Printing the Notice of Delayed Availability

If the teller system is not available, the Teller is responsible for the following:

- Processing the transaction

- Completing a pre-printed Notice of Hold form. A Personal Banker of CXM/CXMII will load the hold in the system

- Attaching a copy of the printout identifying the hold was placed

- Placing the hold notice with daily work for imaging and submission to Deposit Services